One platform, the whole book

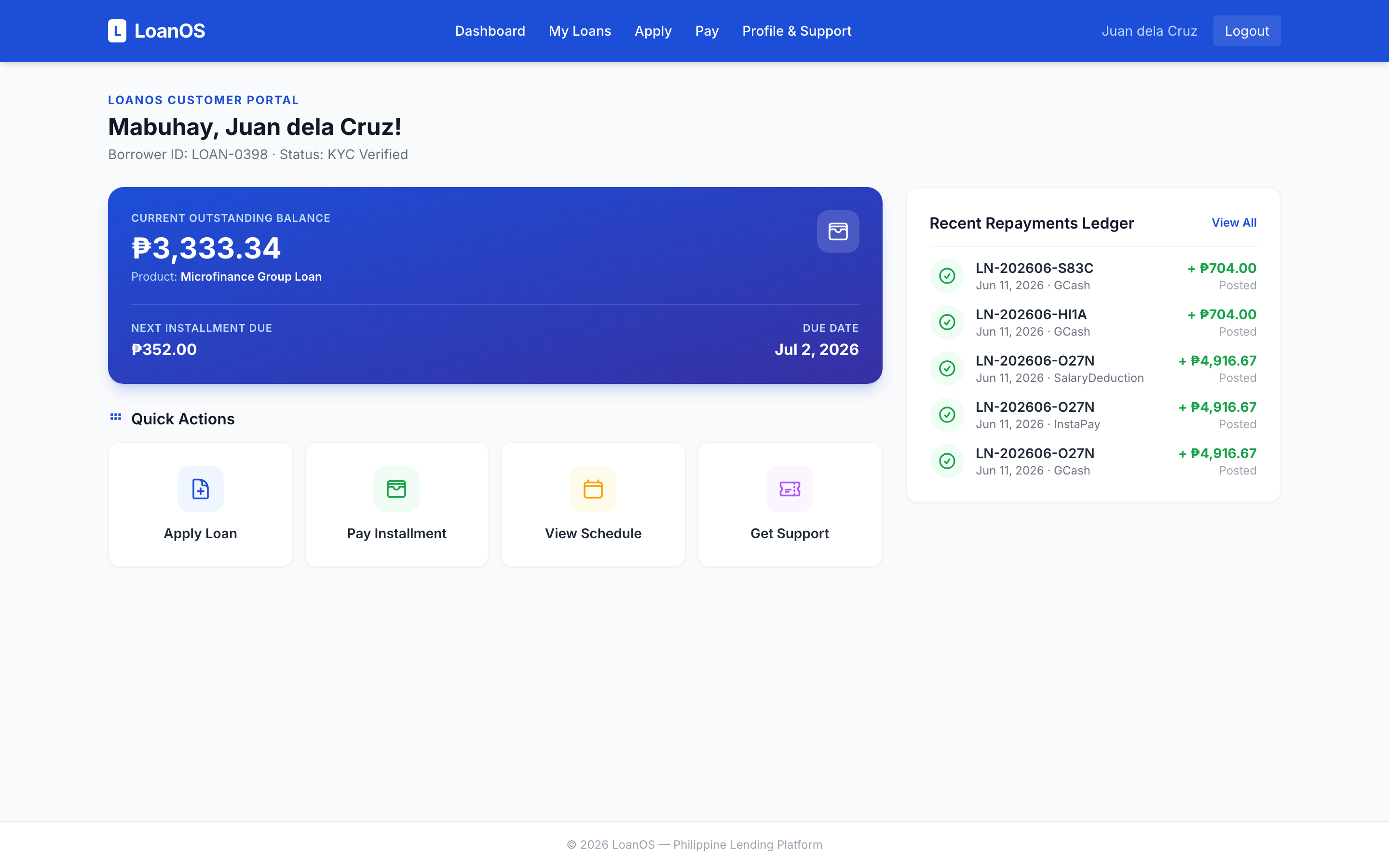

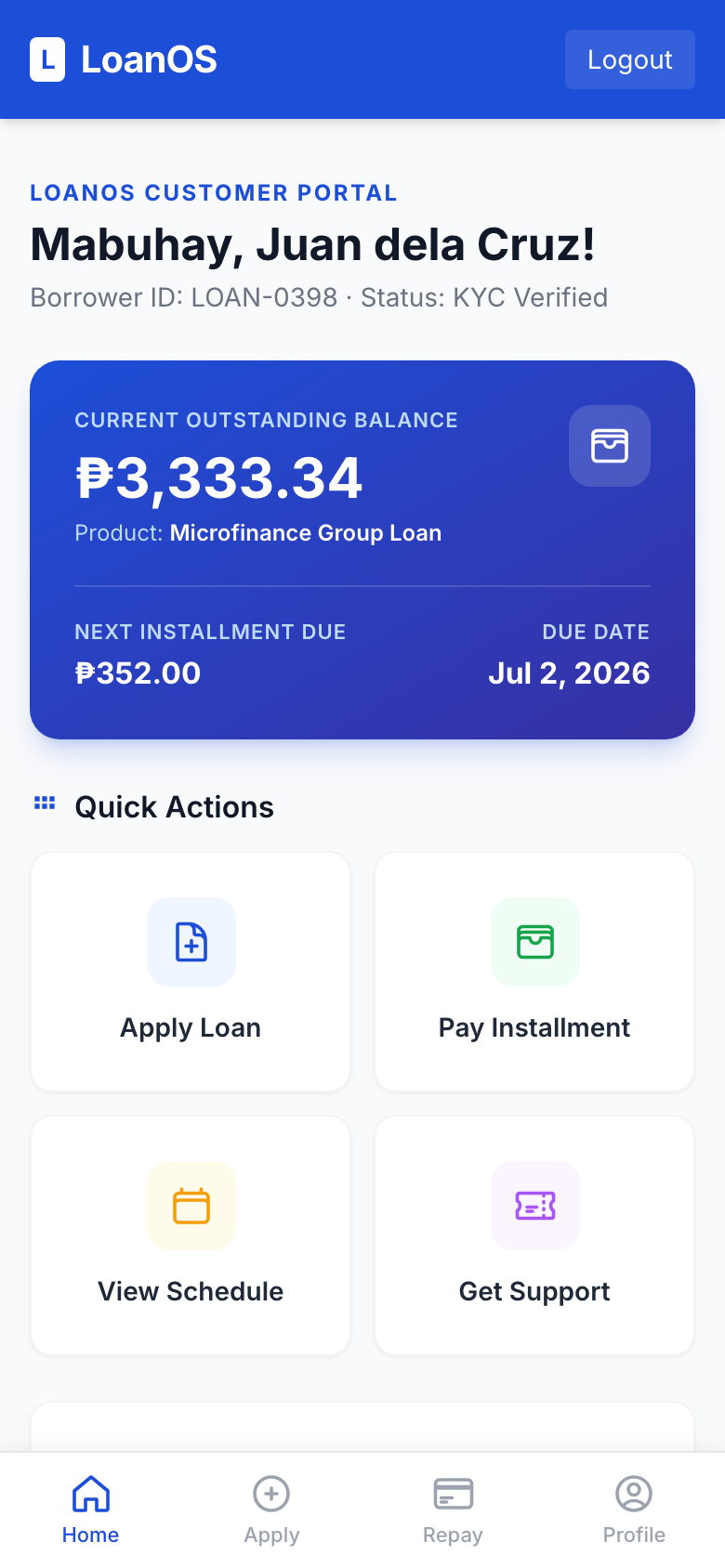

A lending platform, not a loan tracker

Origination is the easy part. This is the rest of it — the ledger, the provisioning, the statutory filings and the collections floor — shaped around how regulated lending actually works here.

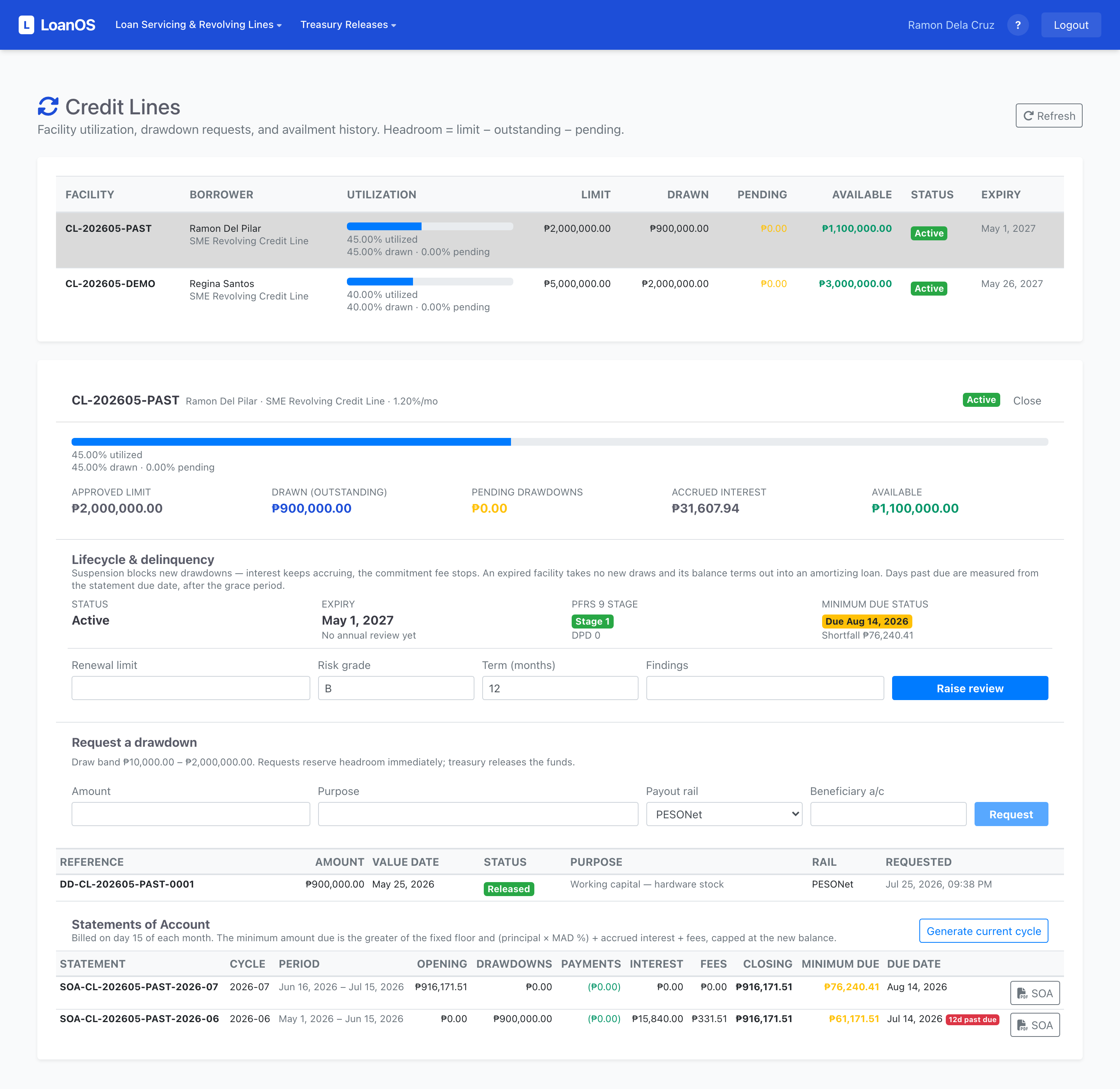

Term and revolving facilities

The flagship: a real revolving credit line — drawdowns under a hard headroom lock, daily interest on utilisation, commitment fee on the undrawn portion, cycle statements with a Minimum Amount Due, and limit re-availment that waits for the bank to clear. Term loans run alongside, untouched.

SEC rate caps, as data

Nominal, EIR, penalty and total-cost ceilings are effective-dated parameters under maker-checker — not constants in someone’s code. Tighten a cap and every product is re-audited; a non-compliant product cannot be saved or activated.

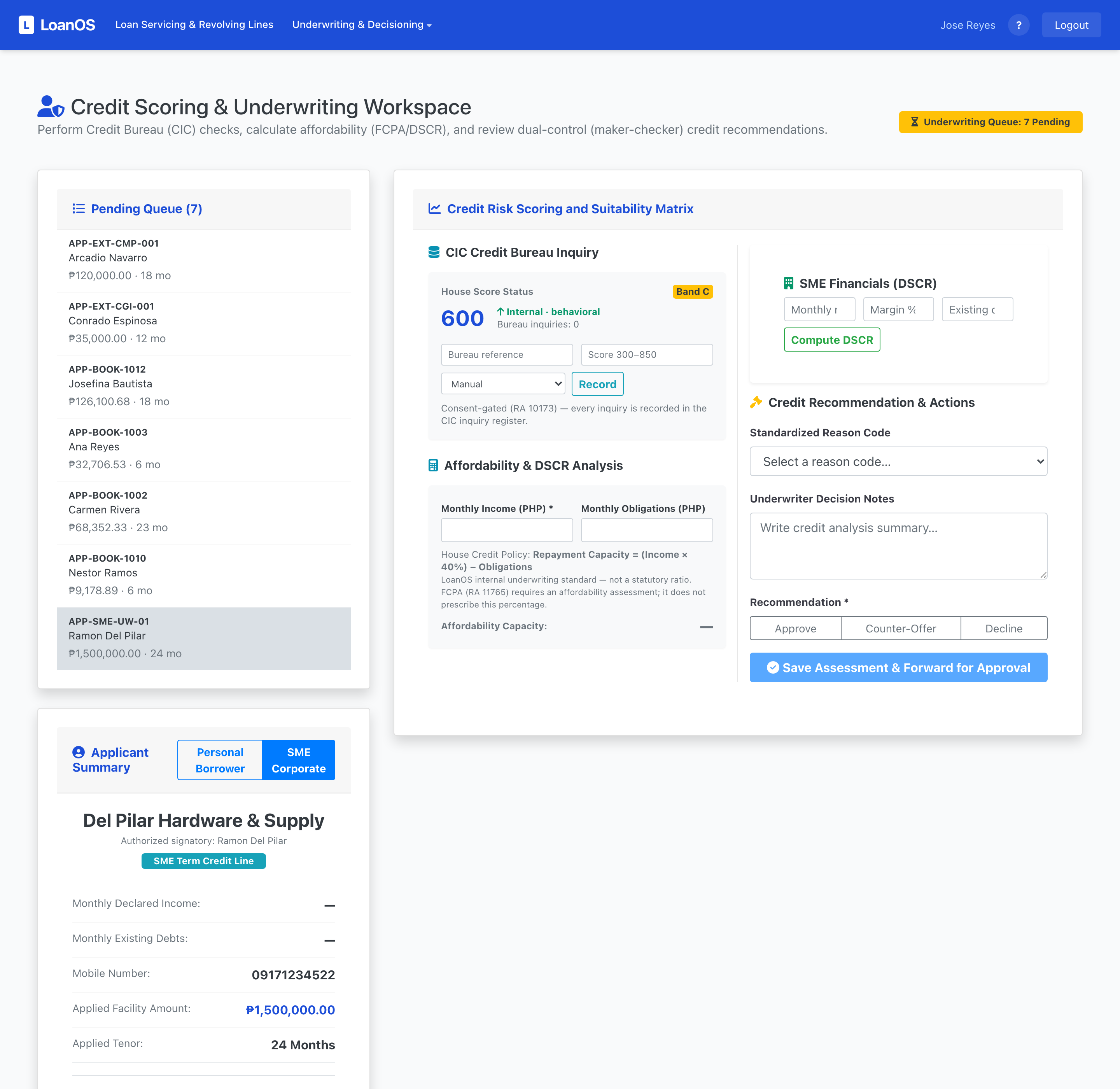

Decisioning with champion-challenger

Policy knock-outs, a versioned scorecard engine and auto-approve / refer / decline bands — plus live A/B traffic splits. Assignment is a deterministic hash, so a re-score never changes a decision, and a challenger cannot be promoted on a cohort too thin to mean anything.

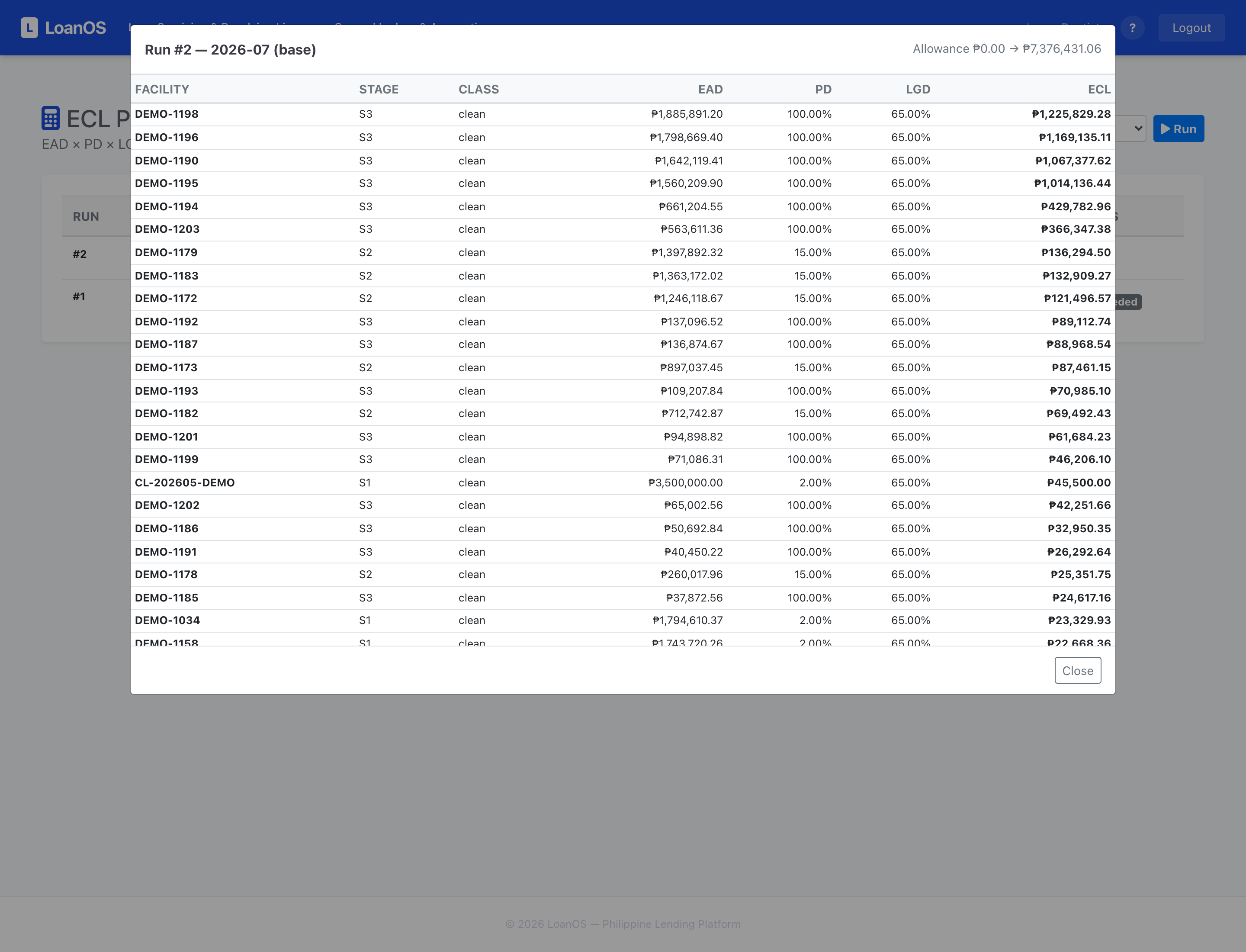

PFRS 9 ECL provisioning

Stage 1/2/3 classification with SICR overlays, effective-dated PD/LGD/EAD tables, monthly provisioning runs that post reverse-and-repost journals, and a movement schedule that ties. Credit lines price EAD as outstanding + CCF × undrawn.

A real general ledger

Five-class chart of accounts, multi-line journal vouchers that cannot post out of balance, event-to-GL mapping with an execution log, period close, trial balance, and off-balance-sheet memorandum accounts for PDCs and pledged mortgages — held out of the statutory books by design.

BIR-ready books

CAS electronic books of accounts, borrower subsidiary ledgers, Form 2307 certificates and tax alphalists — each export hashed into an append-only register. Layouts still awaiting an official spec say so on the face of the file rather than pretending.

Collections that route themselves

PAR-banded worklists, a dialing workbench with promises-to-pay and automatic reminders, capacity-capped queue assignment rules, external agency endorsement with commission accounting, and BP 22 notices with the statutory five-banking-day clock.

PDC vault to clearing

Intake QC that rejects a defective cheque before the borrower leaves, barcode-sealed custody with dual control, banking-day presentment, clearing ingestion with return-reason classification, and a legal evidence pack for prosecution.

Compliance as plumbing

CIC and AMLA reporting, an immutable audit log, branch-scoped row-level access, per-role MFA policy, and a Data Privacy consent ledger whose erasure workflow masks PII while proving the money trail is byte-for-byte intact.